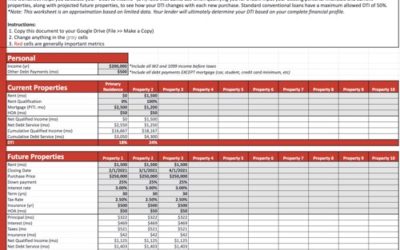

You’ll often hear these terms used interchangeably… but they’re not the same. They simply represent different states you can be in during your loan approval process.

Pre-qualified

Also known as “pre-qualification” or “pre-qual”, this is the most basic state of lender satisfaction. It typically can be done in a day or two with little documentation required. It simply looks at your income vs your liabilities and debt (both current and future) to determine a rough guess of how much home you can afford. Most affordability calculators you can find online will tell you the same thing, the biggest difference is this comes from the lender. You’ll have to ask for it, but they can issue you a simple statement that says you are pre-qualified for a loan up to a certain amount.

Pre-approved

Also known as “pre-approval”, this is a much more in-debt state of lender satisfaction. It requires significantly more documentation and time… typically a week or more. Once approved, and you’ll have to ask for it, a lender can issue you a pre-approval letter for a specific property or loan amount. While an approval letter states that the lender has satisfied all requirements in assessing you for a loan, it doesn’t guarantee you will get the loan or will close without hiccups. There are still things that may come out of underwriting (the final step that makes sure you conform to bank and government standards). However, pre-approval is generally considered to be a good proxy for your ability to close on a loan.